On March 31, 2020, the Department of the Treasury released a sample Paycheck Protection Program (PPP) Loan, providing some (but not all) much needed guidance on the process. A copy of the sample application can be found here.

The application originally uploaded as a sample subject to change. Since then the sample watermark has been removed, but some banking contacts have told us they anticipate additional changes. The guidance on the Treasury website may still be overridden as the program goes live, more regulations come out, or more changes in information are communicated by the Treasury.

Summary of Major New Information

Among the information provided, the biggest revelations are that it appears 2019 data, based on tax forms, will be used in the determination of the loan the amount and that the loan forgiveness will be capped at 25% of non-payroll costs. Further, there is some evidence that lenders will be calculating the amount for borrowers; even in this event, it will be important for borrowers to know what amount they are eligible to receive so that they can make sure they get the proper level of support.

Action Items for Clients

In our prior guide, we gave clients a listing of documents that may be required. This information has been updated and reduced based on the guidance to the following checklist:

This list is subject to change as more information is released.

10 Key Takeaways and Details

1. The Application is short. The Application is 4 pages in total, with the last 2 covering mostly government required notices and some limited guidance on the application. This is certainly welcome.

2. Each 20% or greater owner will need to be listed on the application. This is likely to ease compliance with the SBA Affiliation Rules.

3. A business must answer if they have applied for an Economic Injury Disaster Loan (EIDL) between January 31, 2020 and April 3, 2020, and they must provide details of such loans. There have been a lot of questions about the interplay between these programs. Many applicants have been working or looking to apply for both. We know from the CARES Act the costs cannot be duplicated, but this information makes me wonder if the EIDL application may delay or impair processing of the PPP loan. Further, one of the certifications is that you are not receiving benefits under any other loan under this program. Information and the law previously provided said businesses can apply for both (so long as non-duplicative costs), but this gives us pause on the application and practical limitations as a result.

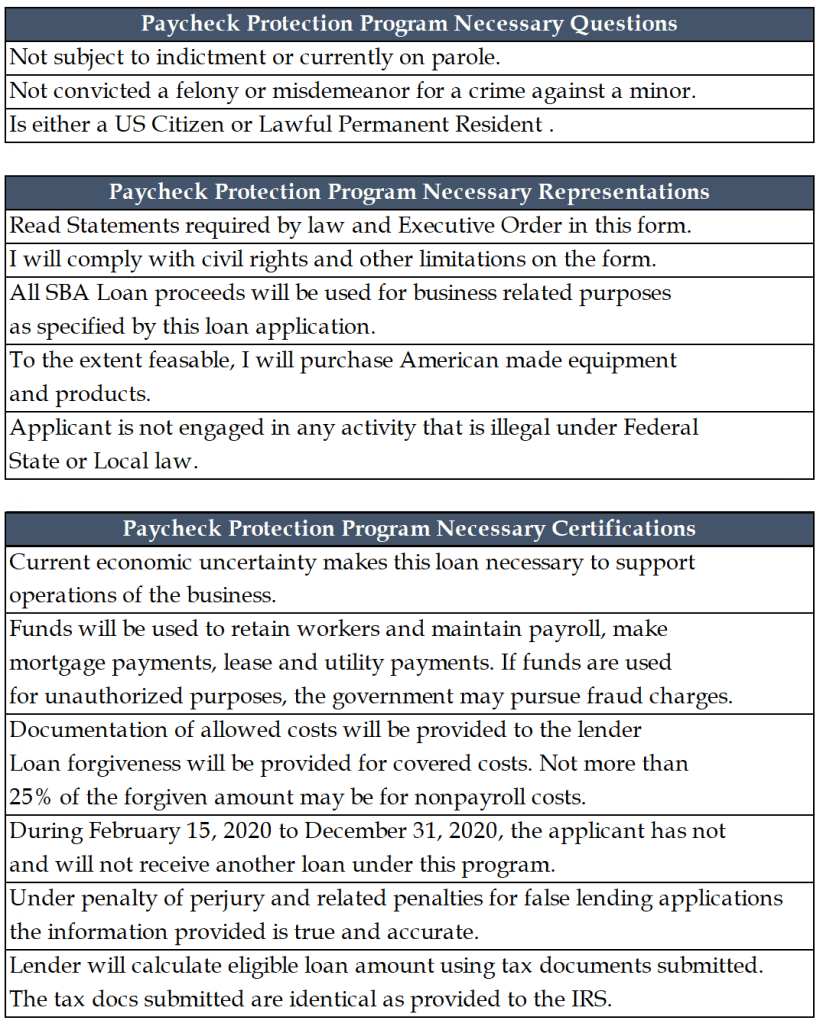

4. Each 20% owner will be required to complete the necessary good-faith certifications and questionnaires. Each 20% owner will need to complete a questionnaire with the following questions (initialed), representations and certifications (initialed):

5. It appears likely that the average annual payroll will be based on 2019 data. The application above requires a certification that loan amount will be calculated based on payroll tax forms provided to a lender. Further, payroll costs as defined on the form indicate “most applicants will use average monthly payroll for 2019”. This is a departure from the literal reading of the law, but also something that may make it easier for both lenders and borrowers.

6. Payroll costs will not include any payments to contractors. The CARES Act was unclear to the ability for businesses who pay contractors; some of the law indicated that these costs may be eligible. The borrower information sheet mentions that contractors can apply for any income from self-employment and does not list them as eligible payroll costs. This most likely means that any contractor you pay (who is self-employed) will have to apply themselves for this program. Allowing businesses to include these costs created a potential double benefit scenario.

7. Forgiveness for non-payroll costs will be capped at 25% of the nonpayroll costs. The program indicates the funds can be used for rent, mortgage interest (the guidance here says mortgage payments, implying full payment) and utilities. However, the borrower information sheet and application indicate that no more than 25% of the forgiven amounts can be for these costs. This was likely put in place to emphasize the use of this loan as an employment retention tool above all else.

8. The program will go live on April 3, 2020 for businesses and April 10, 2020 for sole proprietors & contractors. This is in line with what Secretary Mnuchin had said Monday and expectations from our banking contacts. The delay for contractors and sole proprietors is a new and unexpected wrinkle.

9. The lender may calculate your loan amount for you. Many businesses (and advisors) are working diligently to prepare for these applications and calculation of amounts. One of the certifications and information on the borrower sheet says “lender will calculate the eligible loan amount” using documents submitted. This may relieve, in theory, borrowers from this obligation, but it may not include all eligible costs (as insurance cost may not be reported in a tax form) or 401k matches.

10. The terms of the loans not forgiven have changed. All loans not forgiven will have the same terms – .5% interest rate, per year and a 2-year term. The law allowed for up to 4% and 10 years, so this timeline is more aggressive but cheaper. Loans will accrue interest for the first 6 months and payments will be deferred.

We will be assisting companies in preparing the payroll information needed for the loan application. Please feel free to reach out to us if you would like to engage us to help.

Edward McWilliams, CPA

Partner

Ed is a Partner in the firm’s tax and business advisory practice focusing on providing services to middle market private companies across different industries as well as to early stage startups. Ed has over a decade of experience providing tax and business consulting services to these companies of different sizes and across different industries, bringing a broad and diverse knowledge base and strategic solutions to the many complex issues that businesses face.