The Financial Accounting Standards Board (“FASB”) has issues Accounting Standard Update 2020-07 (“ASU 2020-07”) Not-for-Profit Entities (Topic 958): Presentation and Disclosures by Not-for-Profit Entities for Contributed Nonfinancial Assets, which goes into effect for annual reporting periods beginning after June 15, 2021. Early adoption is permitted. FASB is requiring the standard to be applied retrospectively, which means you need to reflect it for all years presented within your financial statements.

ASU 2020-07 does not change how organizations account for in-kind donations (aka gifts in kind). Organizations still need to evaluate whether donated services are performed by a skilled professional that would have been paid for if not contributed (e.g. construction, legal, accounting, medical) or they enhance organizational assets (such as fixed assets buildings, etc.). The new ASU looks at disclosure, requiring not-for-profits to disclose the following within their financials:

- Present contributed nonfinancial assets as a separate line item in the statement of activities, apart from contributions of cash and other financial assets.

- Disclose:

a.) A disaggregation of the amount of contributed nonfinancial assets recognized within the statement of activities by category that depicts the type of contributed nonfinancial assets.

b.) For each category of contributed nonfinancial assets recognized (as identified in (a)):

- Qualitative information about whether the contributed nonfinancial assets were either monetized or utilized during the reporting period. If utilized, an NFP will disclose a description of the programs or other activities in which those assets were used.

- The NFP’s policy about monetizing rather than utilizing contributed nonfinancial assets.

- A description of any donor-imposed restrictions associated with the contributed nonfinancial assets.

- A description of the valuation techniques and inputs used to arrive at a fair value measure, in accordance with the requirements in Topic 820, Fair Value Measurement, at initial recognition.

- The principal market used to arrive at a fair value measure if it is a market in which the recipient NFP is prohibited by a donor-imposed restriction from selling or using the contributed nonfinancial assets.

There are multiple ways that a not-for-profit can meet the disclosure requirements of ASU 2020-07.

One example is:

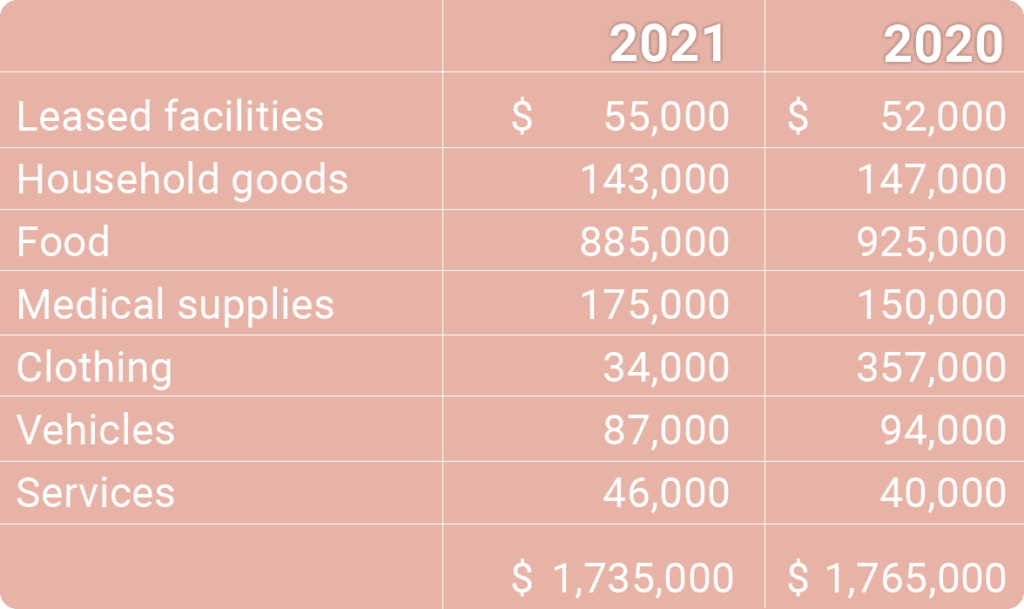

Contributed nonfinancial assets recognized within the Organization’s statement of activities included the following at June 30:

The Organization recognized contributed nonfinancial assets within revenue, including contributed rent, household goods, food, medical supplies, clothing, vehicles, and services. Unless otherwise noted, contributed nonfinancial assets did not have donor-imposed restrictions.

Leased Facilities: The Organization receives the use of 3,500 square feet of retail space in Medford, NY on a donated basis that it utilizes for its food pantry (1,500 square feet) and for its thrift store (2,000 square feet). The space is donated on a month-to-month basis and has been valued at the fair market rent of similar space in the area.

Household Goods: Contributed household goods were used in domestic community development and services to community shelters and low-income families as well as sold within the Organization’s thrift store. During the years ended June 30, 2021 and 2020, $83,000 and $78,000, respectively, were sold within the Organization’s thrift store, with the balance of $60,000 and $69,000, respectively, were used utilized in the Organization’s program activities. Household goods were valued at estimated thrift shop value on date of contribution.

Food: Contributed food was utilized in the following programs: natural disaster services, domestic community development, and distribution through the Organization’s mobile food pantry and food pantries located throughout Suffolk County New York. Food represents food rescue from area restaurants as well as donations from food drives, individuals, and corporate partners. Food is valued at an estimate of $1.85 per pound, which is based upon a feeding America study trended forward to fiscal 2021.

Medical Supplies: Contributed medical supplies were utilized for natural disaster services and the Organizations operations with Long Island based shelters and clinics. The Organization estimated fair value of Medical Supplies on the basis of estimates of wholesale values that would be received for selling similar products in the United States.

Clothing: Contributed clothing were used in domestic community development and services to community shelters and low-income families as well as sold within the Organization’s thrift store. During the years ended June 30, 2021 and 2020, $285,000 and $294,000, respectively, were sold within the Organization’s thrift store, with the balance of $59,000 and $63,000, respectively, were used utilized in the Organization’s program activities. Contributed clothing was valued at estimated thrift shop value on date of contribution.

Vehicles: It is the Organization’s policy to sell all contributed vehicles immediately upon receipt at auction or for salvage unless the vehicle is restricted for use in a specific program by the donor. No vehicles received during the period were restricted for use. All vehicles were sold and valued according to the actual cash proceeds on their disposition.

Services: Contributed services recognized comprise professional services from attorneys advising the Organization on various administrative legal matters. Contributed services are valued and are reported at the estimated fair value in the financial statements based on current rates for similar legal services.

The goal of the new ASU is to provide consistency and transparency in financial reporting surrounding in-kind donations.

This article was also featured in our newsletter NFP Advisor Vol. 23

Erin Gruppe

Staff Accountant

Erin is a member of Cerini & Associates; audit staff where she works with our nonprofit and school district clients. Erin has experience in internal claims auditing and external auditing, including financial statement audits. Erins’ knowledge and experience allow her to provide specific services including systems testing and analysis, internal and external audit functions, and claims audit functions.