There once was a time when employees worked 25-30 years for the same employer and were rewarded for their loyalty and hard work with the benefits that come from an employer sponsored defined benefit (“DB”) plan. Unfortunately, these employees retired at age 65 and had a life expectancy of only a few more years. Up until the 1980’s defined benefit pension plans were the most prevalent and popular retirement plans offered by employers. According to the Bureau of Labor Statistics’ “2018 National Compensation Survey”, only 17% of private-sector workers have access to a defined benefit plan. If you are one of the private-sector employers within the remaining 17% of employers that still sponsor a defined benefit plan, and the cost of sponsoring the plan outweighs the benefits, here are a few options available to you:

1. Freeze Plan

Plans may be frozen at any time for any reason (with 45 days notice to participants)

a.) “Hard freeze” – entry to the plan is frozen by prohibiting new employees from joining the plan and benefit accruals are frozen for existing employees participating in the plan. A hard freeze does not freeze an existing employee, not fully vested as of the freeze date, from continuing to earn vesting credit while working for the organization.

b.) “Soft freeze” – entry to the plan is frozen by prohibiting new employees from joining the plan. Existing employees participating in the plan will continue to accrue pension benefits and vesting service.

2. Change investment strategy

Liability-driven investing (“LDI”) may be implemented by shifting the focus of the plan in order to seek rates of return at or above the market-based growth of the liabilities rather than depending on equity to drive the funding of the pension plan. While LDI reduces the volatility of plan funding, it also has an opportunity cost from foregone equity returns by shifting to LDI.

3. Funding relief

American Recovery Plan Act (“ARPA”) signed into law on March 11, 2021

a.) Single Employer Plans

- Funding shortfalls may be amortized over fifteen (15) years rather than seven (7) years

- ARPA allows for the usage of interest rates based on a 25-year historical average. The higher the interest rates a plan uses, the lower the present value of the liabilities (which is important if you are looking to potentially terminate the plan)

b.) Multi-Employer Plans

- ARPA will establish a fund with the Pension Benefit Guaranty Corporation (“PBGC”), the federal insurance program, to provide assistance (“distressed contribution”) to multi-employer pension plans in danger of insolvency. The “special financial assistance” is designed to cover the amount required to pay all accrued benefits through the last day of the plan year ending 2051.

- A plan can apply for financial assistance through December 31, 2025, and would be eligible based on meeting one of the following conditions:

- It was in critical and declining status in any plan year from 2020 to 2022

- It applied to suspend benefit payments to pensioners under the provisions of the Multiemployer Pension Reform Act (“MPRA”)

- It was in critical status in any year from 2020 through 2022 and had a modified funded percentage of less than 40 percent and the percentage of active to inactive participants in the plan was less than 40 percent.

- It became insolvent after December 14, 2014 and was not terminated by the date on which the new legislation was enacted.

c.) Other Pension Provisions

- Sections 9702, 9703, 9705, 9706, 9707, and 9708 of ARPA provide additional opportunities for relief to both single employer and multi-employer pension plans based on the individual circumstances of the plan.

4. Convert to a Defined Contribution (“DC”) Plan

This is typically done when employers freeze existing defined benefit plans. Employers converting to DC plans may not realize any cash flow savings relief initially, because their existing DB plan must be funded to pay for benefits for employees who are still owed for their pension benefits and the newly created DC plan will also have to be funded (although plan design and funding flexibility exists) at the same time. In the long-term, a DC plan reduces the cost to an employer while also shifts the investment risk to the employee.

5. Convert to a Cash Balance (“Cash”) Plan

Cash plans (also typically done when employers freeze existing defined benefit plan) are really DB plans that require the plan sponsor to be responsible for investing assets and paying the benefits upon retirement, but the formula is based on a set contribution rate for current employees plus a fixed rate of return, which cannot be negative. The benefits received by an employee at retirement are guaranteed and based on their own “account balance”. The Cash plan can be attractive if an employee adopts an LDI investment strategy with a return on investment that exceeds the contribution rate, the true cost to the employer will be less than the contribution rate.

6. Convert to a Cash Plan and Offer a Supplemental DC Plan

Employers offering both of these (again, this is also typically done when employers freeze existing defined benefit plan) plans enable employees to receive a guaranteed benefit amount at retirement from the Cash plan based on the employee’s “account balance,” but also provide supplemental retirement income to the employee. The Cash Plan will provide a conservative investment strategy allowing the employee to take more of an investment risk with their DC Plan investments, which hedges both market risk as well as interest rate risk.

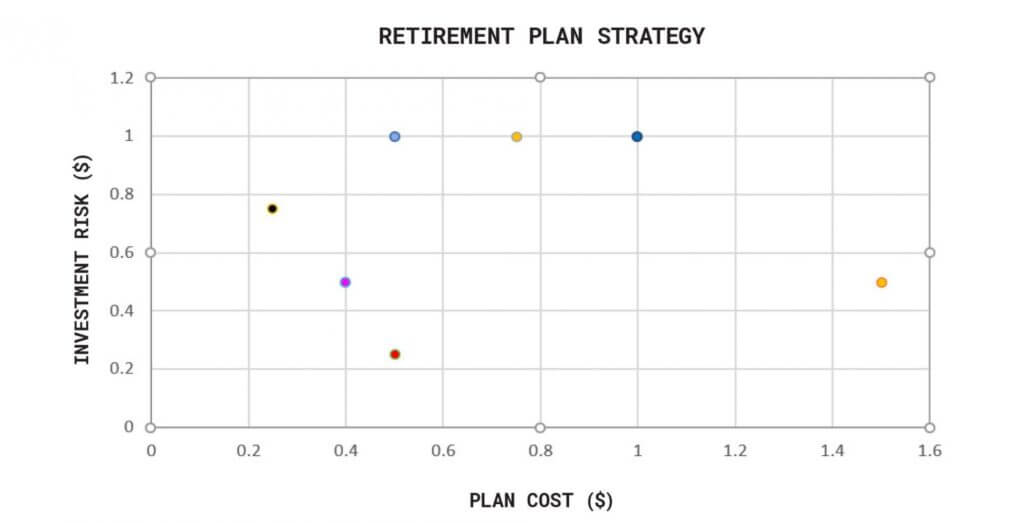

Here’s a visual comparison of all plan options compared to the existing DB Plan (X and Y axis = 1)

If all of the above options have been exhausted, an employer sponsoring a DB Plan may terminate their existing plan via the following options:

1. Standard Termination

This option requires that the plan has sufficient assets (or adequately funded, which means the plan assets is not less than 80% of the plan’s benefits payable/liability as of the liquidation/final distribution date) to satisfy all benefits payable/liability as of the liquidation/final distribution date, regardless if the benefits payable are fully vested (see I.R.C. § 411(d)(3)). If the plan assets are not sufficient to satisfy the plan expense from the plan assets, the plan can (1) fund the expenses by the employer providing a supplemental employer contribution to the plan or (2) the “majority owner” can forego benefits (with spousal consent).

2. Distress Termination

This option is available when a plan does not have sufficient assets to pay all benefit liabilities under the plan. Since underfunded DB Plans are not allowed to be terminated without permission of the PBGC, under ERISA, the PBGC may grant permission to terminate the plan if one of the following situations exists:

a.) Liquidation – the plan sponsor is undergoing liquidation under Chapter 7 of the Bankruptcy Code (or an equivalent state law proceeding).

b.) Reorganization – the plan sponsor has filed a petition under Chapter 11 of the Bankruptcy Code, or similar state law proceeding, and the court determines that, unless the plan is terminated, the sponsor is unable to pay all its debts and will be unable to continue in business outside the reorganization process unless the plan is terminated.

c.) Inability to continue in business – The plan sponsor demonstrates to PBGC’s satisfaction that, unless a distress termination occurs, the plan sponsor will not be able to pay its debts when due and to continue in business.

d.) Unreasonably burdensome pension costs – The plan sponsor demonstrates to PBGC’s satisfaction that the costs of providing pension coverage have become unreasonably burdensome solely as a result of declining covered employment under all of the sponsor’s single-employer plans.

If an employer/sponsor cannot terminate their DB Plan using the Standard Termination method and are unable to demonstrate to the PBGC that a Distress Termination should be granted, these additional options exist:

1. Offer lump sum cash payments to beneficiaries/participants

Often times, terminated vested beneficiaries are targeted for lump sum cash payments, but offering lump sum cash payments to active participants is also a popular strategy. Lump sum cash payments may be made more enticing by offering to roll the lump sum amount over into a participants’ DC Plan account rather than taking the entire payment as a taxable distribution all at one time.

2. Purchase annuity for beneficiaries/participants

For beneficiaries/participants that do not elect to receive a lump sum cash distribution, an employer may purchase an annuity. Depending on the situation, sponsors may be able to finance the annuities by using investments held at a financial institution as “collateral,” for example, if a sponsor holds long-term fixed income assets with a yield rate higher than the anticipated annuity payout rate, some financial institutions may permit sponsors from having to sell their long-term fixed income assets by providing “margin loans” collateralized with the long-term fixed income assets.

3. Change funding strategy

a.) Increase contributions – sponsors may accelerate their contributions to fund the plan (if this is feasible) by increasing discretionary contributions above the statutory requirements.

b.) Issue debt – increasingly common approach, due to the low cost of borrowing, is to issue debt to finance DB Plans and enable sponsors to reach a fully funded position sooner than they otherwise would.

4. Change investment strategy

As previously discussed, sponsors may adopt an LDI strategy if they have not already done so.

Please remember, that while sufficient funding is critical to sponsoring a DB Plan or allowing for the termination of a DB Plan, overfunding the Plan provides little benefit to an employer/sponsor. Once an employer/sponsor contributes to a plan, the funds cannot be accessed until all of the benefits are settled. If assets do remain upon termination, an employer sponsor has the following three options:

1.) Assets can revert directly to the sponsoring employer. Under this approach, the employer is taxed at a 50% rate in addition to any normal corporate tax rates (if applicable).

2.) The employer/sponsor can amend the plan to offer more generous benefits, but this option is rarely taken, particularly since terminating plans have often been frozen for years.

3.) The employer/sponsor can choose to use the remaining funds to benefit the DB Plan participants through a different plan, known as a replacement plan. The participants in the terminating DB Plan must be in the replacement plan, and the employer/sponsor must direct at least 25% of the excess assets toward the other plan in order to reduce the version tax to just 20%.

We know that managing a pension plan can be very complex and time consuming and the laws continue to change, so please feel free to reach out to us as we would be happy to serve as a resource to your organization.

This article was also featured in our newsletter Pension Planner Vol. 3